Payroll in New Zealand

A how-to guide for employers

Payroll can be complex and there are lots of things you need to be aware of when you're running payroll. We’ve put together this comprehensive guide to payroll for New Zealand employers. It’s aimed at both first-time employers who’ve never run payroll before, as well as old hands who want to check a few details.

We hope you find it useful.

Getting started with payroll

If you’re a first-time employer then congratulations – you’re about to start on a great adventure! We can’t tell you how to run your business, but we can give you a few useful tips to make it easy to pay your staff.

- Register as an employer with the Inland Revenue Department (IRD). Register within your myIR account – you’ll need an IRD number to get started.

It’s extremely important to register as an employer – you may be fined by the IRD if you fail to do so.

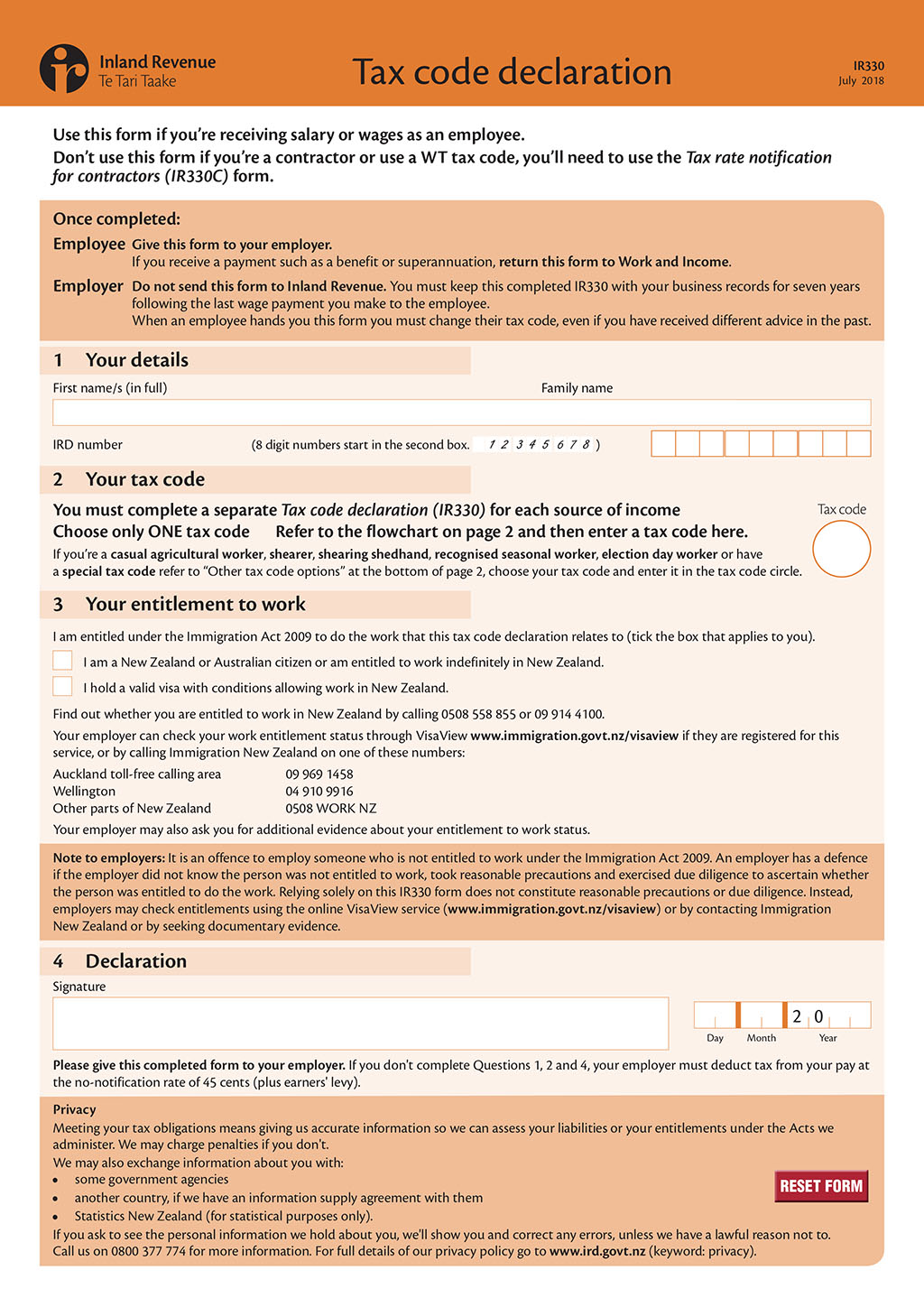

- Get your employees to fill in an IR330 form to determine their tax code. Once you know their code you can work out how much PAYE you need to deduct and whether they need to make student loan repayments.

- Use the KS1 form to automatically enrol them in KiwiSaver if they don’t already belong. Every New Zealand citizen or permanent resident aged 18 to 64 must automatically be enrolled in KiwiSaver – though they can choose to opt out. You should also give them a KiwiSaver information pack (Factsheet KS3) to explain the scheme.

There are currently 28 KiwiSaver providers and your employee can choose to belong to any one of those 27 schemes. They can also change scheme at any time.

- Make the correct deductions from their pay and file the information about these deductions with the IRD within two business days of their payday.

These deductions always include PAYE. They may also include deductions for:

- KiwiSaver contributions

- student loan repayments

- child support payments.

- Calculate your KiwiSaver employer contribution and how much you need to deduct as employer superannuation contribution tax (ESCT).

- Pay the money you have deducted, as well as your KiwiSaver employer contribution, to the IRD by either the 20th of every month or by the 5th and the 20th of the month, depending on the size of your business. Employers whose annual payroll PAYE (including ESCT) is more than $500,000 must make payments twice a month.

Calculating what deductions you have to make

Visit the IRD website for more information about how to calculate PAYE and other deductions.

Employer payroll requirements and responsibilities

As an employer, you have a number of payroll requirements and responsibilities. The first is to pay your staff the minimum wage (or more) at agreed intervals – most employers opt for weekly or fortnightly payments.

Legally, you’re required to pay your staff in cash, but in practice most employees prefer to have a direct credit made into their bank account.

You’re also required to make a number of deductions from your employees’ pay including:

- income tax (PAYE)

- KiwiSaver contributions (if they're a member of KiwiSaver)

- child support payments (if they owe child support)

- student loan payments (if they have a student loan).

You must deduct these sums before you make a payment into your employee’s bank account and then send the deductions to the Inland Revenue (IRD). You send this either once a month or twice a month, depending on the size of your business:

- if your gross annual PAYE (including ESCT) is less than $500,000 you must pay the IRD by the 20th of every month

- if your annual gross PAYE (including ESCT) is more than $500,000 you must pay the IRD by the 5th and the 20th of each month.

All employers, regardless of their business size, must file their employees’ pay information to the IRD within 2 days of every payday - known as payday filing. This replaces the previous monthly filing on the 20th of each month.

Payroll intermediary vs payroll software

How you run your payroll is up to you – many employers do the whole thing using an Excel spreadsheet. But there are two ways you can make the process easier:

- Use a payroll (or PAYE) intermediary which provides all your payroll services. New Zealand has numerous payroll intermediaries – including us, Thankyou Payroll.

- Use payroll software that has been developed so that you – or another staff member or an accountant – can manage your payroll and filing in-house.

Payroll intermediaries make payroll easy

Using a payroll intermediary like Thankyou Payroll makes payroll super easy. All you need to do is send us your employees’ gross payment and any other relevant information (such as how much leave each employee has taken during that pay period, and information about new or departing employees) and we’ll do the rest for you.

Why use payroll software?

Payroll software allows you to run your own payroll. It means either you or another staff member is responsible for the entire process – and also responsible for correcting any mistakes.

There are some advantages to using software to do your own payroll. The main one is that you pay a set amount for payroll software no matter how many employees you have.

Payday filing

Payday filing was introduced on the 1st April 2019 and requires businesses to file employees’ pay information to the Inland Revenue (IRD) every payday.

When do I have to file?

Under the payday filing system, you’ll have to file your employees’ pay information within two working days of each payday. If you pay weekly, that means you’ll have to file the information to the IRD every week, instead of the 20th of each following month as is has been.

Electronic filing compulsory for larger enterprises

Electronic (online) filing will be compulsory for all employers whose annual PAYE and ESCT deductions (combined) are more than $50,000 a year. You must have a myIR account to do electronic payday filing.

Paper filing is only available to employers whose annual PAYE and ESCT deductions total less than $50,000 a year. If you chose to do paper filing, you can either:

- file twice a month (on the 15th and the last day of the month)

- file within 10 working days of payday.

What about IRD payments?

Payday filing only applies to your employees’ pay information, not to your IRD payments. You’ll still be able to make a single monthly payment on the 20th of each month, or two payments on the 5th and the 20th of the month, depending on the size or your enterprise.

What information do I have to file?

Under the payday filing system you have to file all the information you filed previously, as well as some additional information. All this information must be filed within two days of each payday.

That means that, just as you did previously, you’ll have to file information about:

- PAYE payments

- KiwiSaver payments

- student loan repayments

- payroll giving donations and tax rebates

- any other deductions.

With payday filing, you’ll also have to file information about:

- ESCT (employer superannuation contribution tax) for each employee

- the pay period start and end dates

- the pay cycle (how often it occurs)

- the payday date

- new and departing employees.

Filing information about new or departing employees

Payday filing requires you to file the following information about new or departing employees:

- their start and end dates

- their contact details

- their date of birth (if they give it to you).

PAYE

Employees earning a wage or salary are taxed directly from their pay. This is known as PAYE (pay as you earn). As an employer, you're responsible for deducting and paying PAYE income tax on your employees' behalf.

Calculating PAYE

The amount of PAYE you deduct depends on your employee’s tax code and how much they earn. To work out what you need to deduct, use IRD’s PAYE/ KiwiSaver deductions calculator.

KiwiSaver and other non-PAYE deductions

As well as deducting PAYE from your employees’ salary you may also have to make deductions for:

- KiwiSaver or complying fund

- student loan repayments

- child support payments

- IRD debt repayments.

All these deductions (including PAYE) must be paid to the IRD by the 20th of the month (or the 5th and the 20th if you opt to do twice monthly payments, or if you’re a large organisation with over $500,000 in PAYE/ESCT per annum).

KiwiSaver – an opt-out superannuation scheme

KiwiSaver is not compulsory, but all eligible employees who are not enrolled in KiwiSaver must be automatically enrolled when they start a new job. Eligible employees are all employees aged 18 to 64 who are either New Zealand citizens or permanent residents.

Use the KS1 form to enrol new members into the scheme.

Employees can choose to opt out of KiwiSaver once they have worked for you for 14 days. They have another 6 weeks to opt out; after that they can apply for a late opt-out. It’s also possible for employees who are already enrolled in the scheme to apply for a “contributions holiday”.

Employees aged 65 or older who have belonged to KiwiSaver for five years or more are not required to keep making payments.

Different levels of employee KiwiSaver contribution

Employees can choose three different levels of KiwiSaver payments – 3%, 4%, 6%, 8% or 10% of their before-tax pay.

Get them to use the KiwiSaver deduction form (KS2) to choose what level of payment they want to make.

As an employer you can have a preferred KiwiSaver provider. Your employees can also choose their own provider. If they don’t have a nominated provider IRD will automatically enrol them in one of the nine government-appointed default providers.

To work out how much you need to deduct, use IRD’s PAYE/KiwiSaver deductions calculator.

Employer KiwiSaver contribution

As an employer, you must contribute another 3% (minimum) of your employee’s gross pay to their KiwiSaver account.

Download the KiwiSaver employer guide (KS4) for more information about your KiwiSaver responsibilities.

Employer superannuation contribution tax (ESCT)

The employee’s contribution to KiwiSaver is not taxed. However, the employer’s contribution is taxed – this tax is called employer superannuation contribution tax (ESCT). The level of ESCT varies according to how much the employee earns. It ranges from 10.5% to 33%.

Visit the IRD website for more information about ESCT.

Student loan repayments

Anyone with a tax code that ends in SL and who is earning more than $19,448 gross a year ($374 a week) must make student loan repayments. In most cases you will need to deduct 12 cents for every dollar they earn above $19,448.

Secondary income is also subject to student loan repayments.

Visit the IRD website for more information about student loan repayments and how to calculate them.

Child support payments

As an employer you are required by law to deduct child support payments from an employee’s wages if the IRD tells you to do so. You must keep deducting these payments until the IRD tells you to stop.

The IRD will tell you how much to deduct and how to make and pay the deductions.

It’s important that you respect your employee’s right to privacy when it comes to child support payments.

Payslips

You’re not legally required to provide your employees with a payslip each time you run a payroll unless it’s in your employment agreement. But giving your employees a payslip is a useful way to make sure you both understand how their pay is made up.

A payslip can include:

- how many hours the employee worked during that pay period

- their gross pay for that pay period

- their pay rate

- their PAYE deductions

- any other deductions you made (such as KiwiSaver or student loan payments)

- how much annual leave they took, and how much they have owing

- how much sick leave they took and how much they have owing.

A payslip can be anything from a handwritten document to an app your staff download onto their phones – it’s up to you to decide how you want to issue them.

Most payroll intermediaries provide payslips as part of their service. At Thankyou Payroll we email your employees their payslip and send a summary of these to your administrator. Employees can also download a free app where they can find information about their income, leave balances and payroll giving totals.

Timesheets

Timesheets are a useful way of recording how many hours each employee has worked and what leave they’ve taken (including annual holidays – often called annual leave – and sick leave).

It’s important to break your timesheets down by day. Without daily records it’s almost impossible to accurately calculate annual holidays using the rate set by the Holidays Act 2003.

It’s up to you what kind of timesheets you use. Possibilities include:

- having a book where each employee records their hours

- issuing staff with individual timesheets (there are plenty of templates available to download online)

- getting your staff to email their hours to you and entering them into a spreadsheet

- setting up an online system so that staff can enter their hours into it directly.

Whatever system you choose it’s important to stay up to date so you don’t lose track of who worked when.

Annual holidays and other leave

Employees are legally entitled to several different types of leave including:

- annual holidays (often called annual leave) – a minimum of four weeks a year after 12 months of continuous employment. That is equivalent to 20 days for full-time employees. Part-time employees are also entitled to a minimum of four of their usual working weeks each year

- sick leave – a minimum of five days a year, available after 6 months of continuous employment

- bereavement leave – a minimum of three days per death of a spouse or partner, parent, child, sibling, grandparent, grandchild, or spouse or partner's parent. One day, at the employer's discretion, on the death of another person, available after six months of continuous employment

- domestic violence leave – from 1st April 2019, a minimum of ten days to deal with effects of domestic violence. At the employer’s discretion, a short-term variation to their working arrangement can also be agreed.

As an employer, you can agree to let your workers anticipate these three kinds of leave before they have met the continuous-employment requirements. Make a note of this in your records to ensure you don’t lose track of what leave they have taken.

Annual leave must be paid at the higher of either an employee’s average weekly pay or their ordinary weekly pay.

For most employees sick leave and bereavement leave are paid at their normal hourly rate for the number of hours they were scheduled to work that day. For employees who work irregular hours, it’s paid at their average daily rate.

Accumulating and cashing out annual holidays

Some employers let their staff accumulate annual holidays (annual leave) over several years. Your staff are also legally entitled to cash out one week of annual holidays a year if they choose to.

There’s no legal limit to how many years worth of annual holidays your staff can accumulate, however it can be a liability on the company to have employees carrying a large annual leave accruement balance. For this reason, Thankyou Payroll recommends having a policy for a maximum of weeks of annual leave that each employee can accrue.

There are a couple of reasons for this:

- Carrying accumulated annual holidays is a financial liability – if that person resigns you will have to pay out their outstanding leave in full which may put a dent in your budget.

- It’s important for work-life balance that your employees actually take time off – they’ll be more productive and refreshed if they have a decent holiday every year.

Accumulating sick leave

Your employees are legally entitled to accumulate 20 days of sick leave. You may reach an agreement that allows them to accumulate more than 20 days.

Your employees cannot cash out unused sick leave, and they are not paid for unused sick leave in their final pay.

Final pays

It’s common practice to make a final pay on an employee’s last day of work. Employees must receive their final pay on the next payday for their final period of work.

A final pay includes:

- payment for all the hours worked since their last pay until the end of employment

- payment for any unused annual holidays. This includes both allocated annual holidays from the previous 12 months, and any alternative holidays they have accrued since then.

Good records are the secret to taking the pain out of final pays. They make it easy to calculate exactly how much annual leave an employee has owing to them so you can include it in their final pay.

Two little-known rules about final pays that may trip you up

There are a couple of things that can trip you up when you’re calculating the value of outstanding annual holidays. If you’re not familiar with these you may end up making an expensive mistake – another reason to use a payroll intermediary!

- If your employee has worked for you for 12 months or more, they may be entitled to be paid for public holidays that occur soon after they have finished working. This happens because outstanding annual holidays effectively extend their period of employment with you. For example, if your employee’s last day of work is the day before Good Friday and they have two weeks (10 days) of annual holidays owing to them, they must be paid for those 10 days, plus another two days for the public holidays on Good Friday and Easter Monday.

- Any outstanding annual holidays continue to attract an 8% annual holiday entitlement. That means that if your employee has 80 hours (two weeks) of allocated annual holidays, you must pay them for those 80 hours, plus another 6.4 hours (8% of 80 hours).

Public holidays

New Zealand has 11 public holidays a year. These are additional to annual holidays and employees are entitled to public holiday benefits as soon as they start working for you.

The rules around public holiday benefits are covered by the Holidays Act 2003. They can be complicated, particularly if you employ casual or part-time staff. But in the majority of cases the following rules apply:

- If a waged employee works on a public holiday they must be paid time-and-a-half for every hour they work. They are also entitled to an ‘alternative holiday’ – one day off in lieu to be taken at an agreed time.

- If a salaried employee works on a public holiday they are also entitled to be paid time-and-a-half for every hour they work, as well as an ‘alternative holiday’.

- If an employee, either waged or salaried, is normally scheduled to work on the day of a public holiday but they are not required to work on it, they are paid their usual daily.

- If an employee, either waged or salaried, is not normally scheduled to work on the day of a public holiday and they are not required to work on it, they do not get paid for the public holiday (for example, if they normally work Tuesday to Saturday and the public holiday falls on a Monday).

Payroll giving

Payroll giving allows your staff to donate directly from their pay and get an immediate 33.33% tax credit. They can make the donations every payroll or choose to donate less often.

At Thankyou Payroll we have a strong commitment to giving, and we love payroll giving because it provides an easy giving pathway. Our employee app means that staff can easily keep track of their giving and check out their giving totals.

Payroll giving is easy if you use a payroll intermediary like Thankyou Payroll – we’ll take care of the whole process for you.

If you organise your own payroll and you have staff who want to take part in payroll giving you’ll need to set up a system to:

- deduct the nominated donation from your employee’s salary for each payroll

- calculate the 33% tax rebate on the donation and reduce their PAYE by that amount

- file information about the tax/charitable rebate to the IRD – you’ll need to do this at the same time as you file other employee payroll information

- ensure you pay the donation to the employees chosen charity within a specified period ( see the IRD website for the current payment schedules). You’ll have two months and two days after the end of the pay period to pay the donation.

Wages vs salaries

Most employees are paid either wages or a salary.

Wages are usually based on an hourly rate and paid according to the number of hours the employee works. All staff aged 15 to 65 must be paid at least the minimum wage (currently $18.90).

You may agree to pay your employee penal rates (extra pay) for working extra days, or particular shifts or days. Payment for working on public holidays is covered by the Holidays Act 2003.

A salary is a fixed amount per year. Your employee receives the same weekly salary regardless of how many hours they work. You may also agree to time off in lieu (TOIL) if they work more than an agreed number of hours.

The decision about whether you pay wages or salaries is entirely up to you and your employee. However, there are some logistical advantages to having staff on annual salaries. They’re very straightforward to pay and they make it easy to manage annual and public holidays.

Any questions?

Please send us an email or call 04 488 7531.

Get started now!

Easy setup, no hidden fees, no contracts. We’ll take your payroll and give you back your time.